Deciphering Treasury bonds

- Markets & Investing

- Article

Why Treasury bonds could be beneficial in the current climate.

Puzzled by the Treasury bond market? You’re not alone. While considerations around buying and selling stocks and mutual funds are relatively easy to understand – buy low, sell high, avoid high-fee funds – Treasury bond purchase considerations are not quite as straightforward. For example, as bond prices go up, yields go down. Wait, what?

But an explanation of these concepts can help you confidently wade into Treasury bond trading and take advantage of the still favorable bond market in 2024.

What is a Treasury bond?

U.S. Treasury bonds are debt issued by the U.S. Treasury Department and backed by the U.S. government. The purchaser of a bond in effect loans the government money, and the government pays a fixed interest rate to the bond holder until maturity, when the government pays the full face value of the bond.

The bond market is segmented based on bond type and maturity. Treasury bills have maturities up to one year. Because they’re a short-term investment, they don’t pay interest. Instead, they’re issued at a discount to their face value, and when they mature, holders are paid face value. In contrast to Treasury bills, Treasury notes and Treasury bonds pay interest, which is referred to as a coupon payment. Treasury notes are short- to mid-term securities with maturities ranging from 1 year to 10 years, while treasury bonds mature in either 20 or 30 years.

Why is the 10-year T-note an economic bellwether?

The 10-year Treasury note serves as an important indicator that helps us understand what’s happening in the financial world. It provides a signal of the market’s expectations for inflation and the overall economic health. And it acts as a benchmark for setting interest rates on a wide range of financial products, from mortgages to corporate debt. It also has global significance as it’s the most widely used interest rate benchmark for pricing all risk assets worldwide. When you see the 10-year Treasury yield go up or down it’s a reflection of how investors are feeling about the economy and where they think it’s headed. Declines in yields generally indicate an economic slowdown or lower inflation. While gains signal higher growth or inflation.

However, rising yields might also result during high inflation when investors won’t buy bonds unless their price falls to offset the inflation. Thus, high yields don’t always indicate desirable economic circumstances.

Investors compare the return on a 10-year Treasury note to other debt instruments. If the yields are high relative to these other instruments, investors tend to favor Treasuries. As a result, the other debt instruments must increase their interest rates to attract investors.

Therefore, when the yields for 10-year Treasuries rise, the rates for mortgages and car loans can also increase, directionally tracking the movement in 10-year Treasuries. Similarly, when yields fall, the rates for mortgages and car loans can also decrease. This relationship illustrates how the 10-year Treasury note yield serves as a benchmark in the financial market.

10-year Treasury yields remain an attractive opportunity

The 10-year Treasury yields peaked in the third quarter of 2023 but remain high. At the same time, as the market anticipates interest rate cuts, 10-year Treasury yields may begin to fall. What does all this mean for investors curious about buying Treasury bonds with fixed rates and predictable returns? Now might be a good time to consider buying a 10-year Treasury for two reasons.

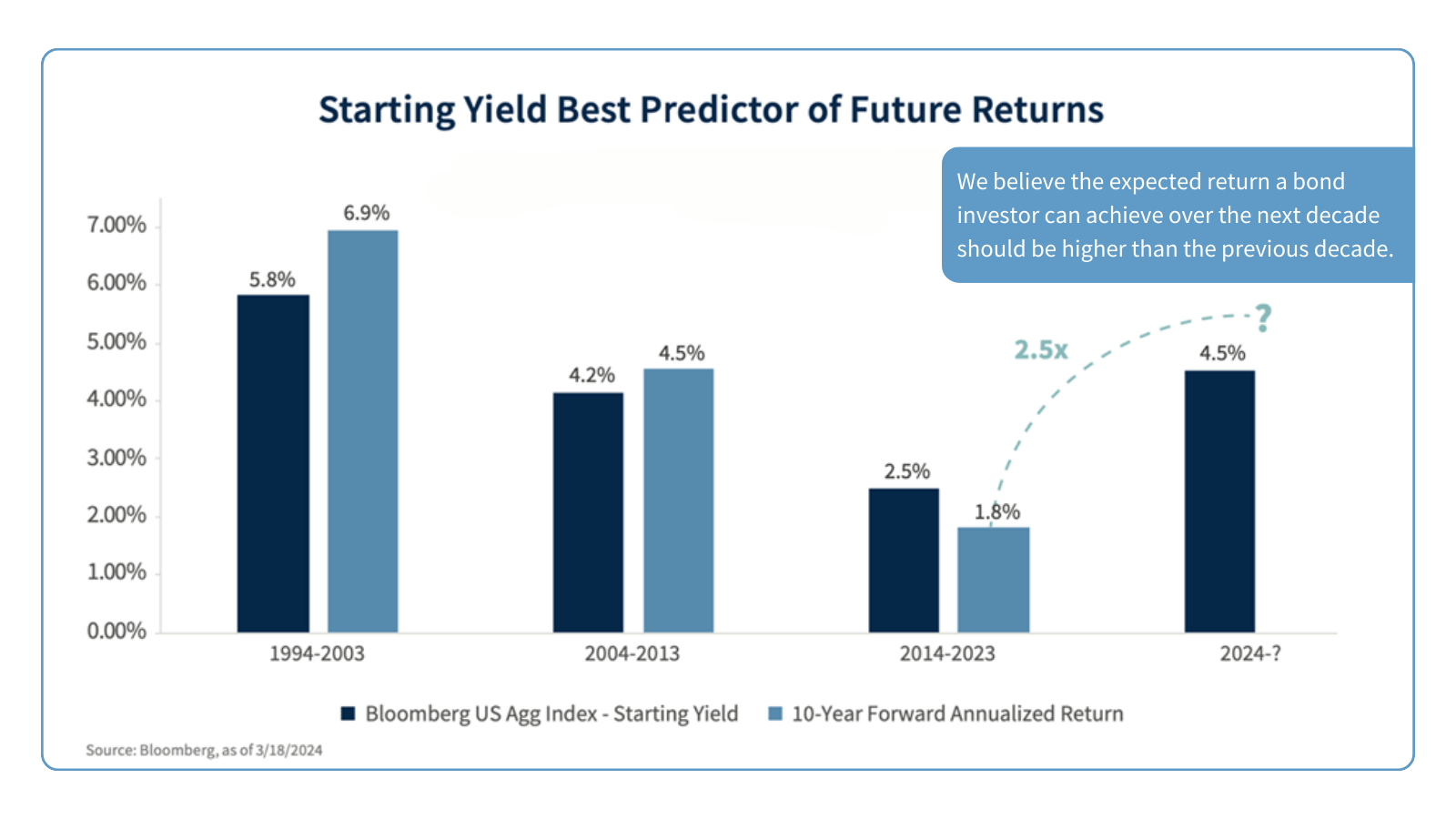

First, treasury bond yields are still relatively high compared to what they have been in the past decade.

Second, the starting level of bond yields is the single best predictor of a bond’s total return over longer periods of time. Considering these two factors together, the relatively high yields available in 2024 mean that Treasury bonds are worth a close look.

Treasuries are a strong fixed-income investment for those who prefer low-risk options that have a predictable return stream. While high-interest savings accounts are presently offering similar yields, the interest rates you earn from these savings accounts will fall if the Federal Reserve cuts interest rates. In contrast, Treasury bonds purchased now will maintain the same rate of interest even if the Fed lowers rates.

Of course, how much an individual should invest in bonds depends upon several factors, including their goals, retirement status, and risk appetite. Investors should speak with their financial advisor to carefully assess market dynamics and consider whether Treasury bonds generally make sense and what mix of durations would best align with their investment aims.

Whatever you decide, if you talk to your advisor, you won’t get lost in the intricacies and counterintuitive qualities of bond investing.

Sources: im.natixis.com, smartasset.com, indiainfoline.com, Nerdwallet, investopedia, treasurydirect.gov, Reuters Expressions of opinion are as of this date and are subject to change without notice. The value of fixed income securities fluctuates, and investors may receive more or less than their original investments if sold prior to maturity. Bonds are subject to price change and availability. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Asset allocation and diversification do not guarantee a profit nor protect against loss.